LA-Z-BOY (LZB)·Q3 2026 Earnings Summary

La-Z-Boy Beats on Revenue and EPS as Retail Expansion Drives Double-Digit Growth

February 17, 2026 · by Fintool AI Agent

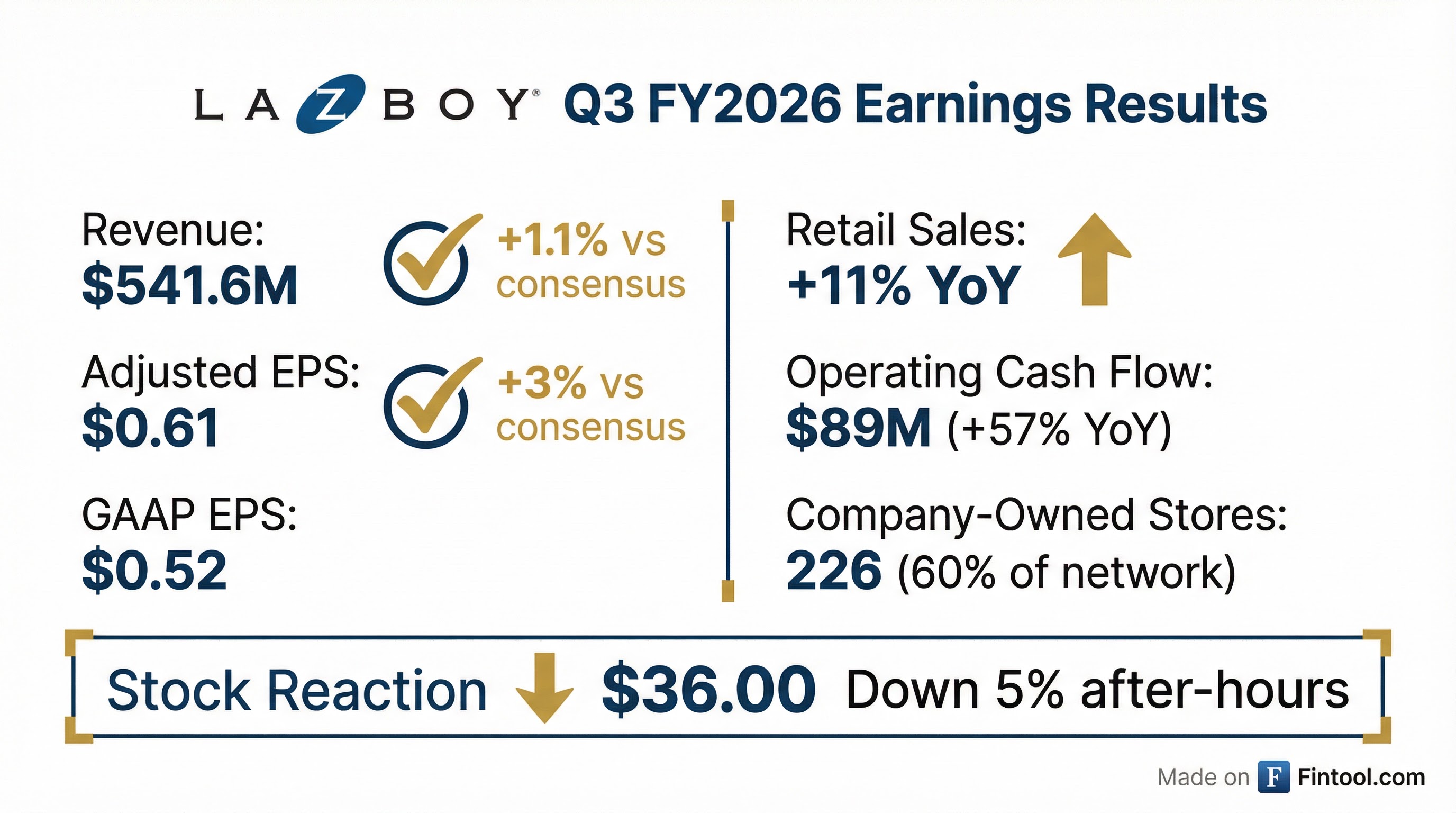

La-Z-Boy (NYSE: LZB) reported Q3 FY2026 results that topped consensus on both revenue and adjusted earnings, powered by double-digit growth in its retail segment. Revenue rose 4% year-over-year to $541.6 million, beating analyst estimates by 1.1% . Adjusted EPS of $0.61 exceeded the $0.59 consensus by 3.4% . Despite the beat, shares fell approximately 5% in after-hours trading to $36.00 as investors digested cautious Q4 guidance citing macroeconomic uncertainty and weather impacts.

Did La-Z-Boy Beat Earnings?

Yes — La-Z-Boy beat on both revenue and adjusted EPS.

*Values retrieved from S&P Global

GAAP EPS of $0.52 included $0.09 per share in charges related to the planned closure of UK manufacturing operations . Operating cash flow surged 57% year-over-year to $89 million, demonstrating strong cash conversion even amid strategic investments .

The company has now beaten consensus on adjusted EPS in 5 of the last 8 quarters, though the magnitude of beats has been modest.

What Changed From Last Quarter?

Several key developments emerged this quarter:

Accelerated Retail Expansion: The company opened 4 new stores in Q3 and added 29 net stores over the trailing twelve months (16 new, 17 acquired, 4 closed). Company-owned stores now represent ~60% of the total network — an all-time high — up from roughly half just a few years ago .

Portfolio Rationalization Progress: La-Z-Boy made significant strides on its Century Vision strategy to focus on core branded upholstery:

- Successfully integrated a 15-store acquisition in the Southeast

- Announced closure of UK manufacturing (production to cease by fiscal year end)

- Completed sale of Kincaid upholstery business post-quarter

- Signed letter of intent to sell wholesale casegoods businesses (American Drew and Kincaid)

Distribution Transformation: The western U.S. phase of the distribution and home delivery transformation project was completed, though investments continue to pressure wholesale margins .

How Did Each Segment Perform?

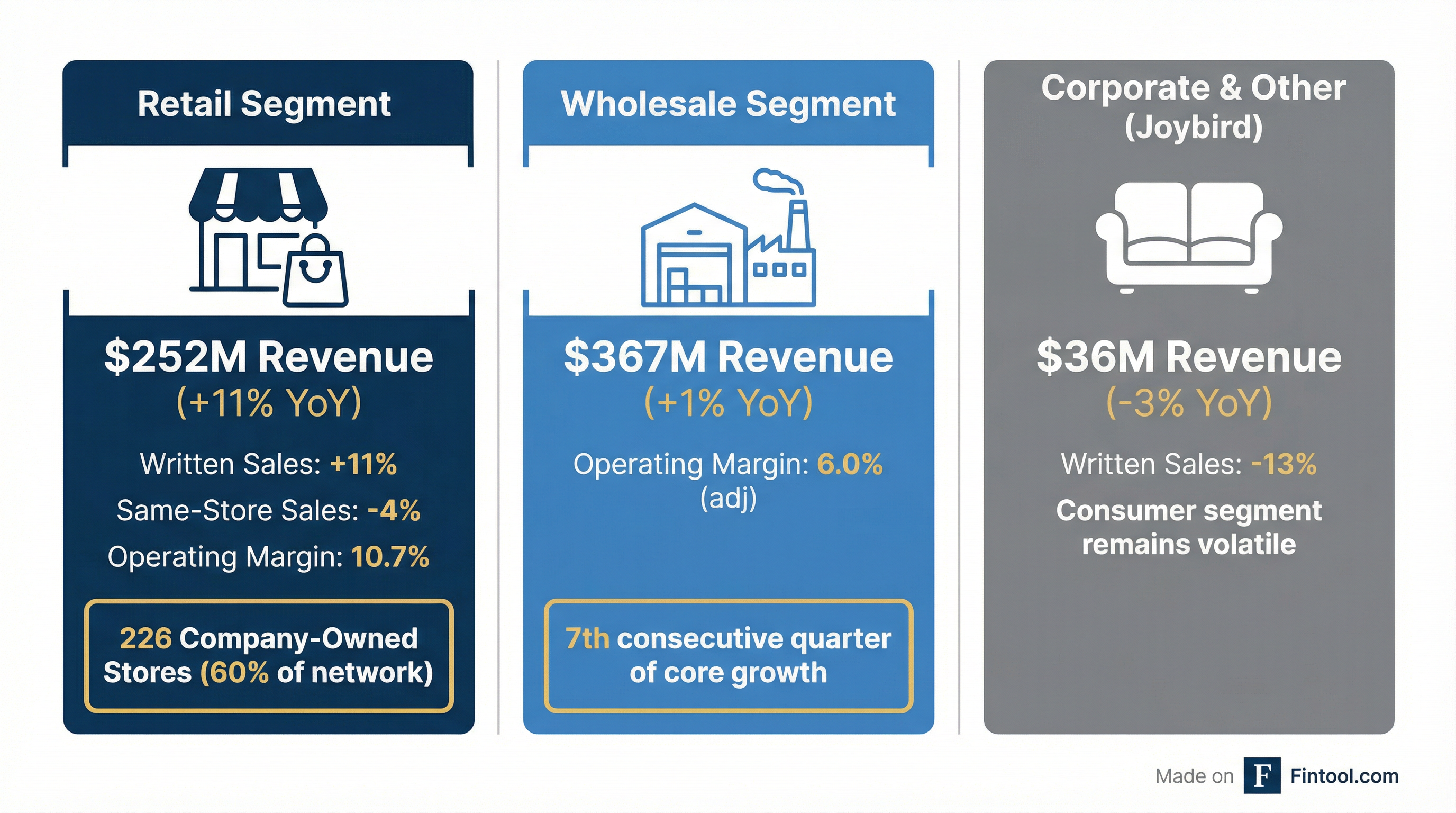

Retail Segment

The star performer, with delivered sales up 11% to $252 million driven by acquired and new stores . Written sales also increased 11%, signaling continued momentum in the backlog .

However, same-store sales declined 4% as lower traffic offset higher conversion rates, average ticket, and design sales . Management noted that same-store trends were strongest in January before adverse weather slowed traffic late in the month .

Adjusted operating margin held flat at 10.7%, as accretion from acquisitions was offset by new store investments and fixed cost deleverage .

Wholesale Segment

Sales increased 1% to $367 million, marking the seventh consecutive quarter of growth in the core North America La-Z-Boy wholesale business .

Adjusted operating margin declined to 6.0% from 6.5% a year ago, driven primarily by distribution transformation investments and unfavorable foreign exchange rates .

Joybird (Corporate & Other)

The direct-to-consumer Joybird brand continues to struggle in the current macro environment:

- Written sales declined 13%

- Delivered sales down 3% to $36 million

- Segment operating loss increased on expense deleverage

Management characterized this consumer segment as "particularly volatile against the current macroeconomic backdrop" .

What Did Management Guide?

CFO Taylor Luebke provided Q4 FY2026 guidance reflecting continued macro caution:

The guidance reflects "a continued cautious view on the macroeconomic backdrop as well as the short-term impact of recent adverse weather events" .

Implied FY26 Full Year: Based on YTD results and Q4 guidance midpoint, full-year revenue would be approximately $2.13 billion, roughly in line with the $2.14 billion consensus.*

*Values retrieved from S&P Global

How Did the Stock React?

La-Z-Boy shares closed at $37.93, down 1.1% during the regular session before results were released. In after-hours trading, the stock fell to $36.00 — down approximately 6% from the prior close of $38.34.

The negative reaction despite the beat likely reflects:

- Cautious Q4 guidance with operating margin below year-ago levels

- Joybird weakness continuing with no clear inflection

- Same-store sales declining despite strong new store growth

- Macro uncertainty weighing on consumer discretionary names

Year-to-date, LZB shares are roughly flat after rallying ~20% from October 2025 lows.

What's the Bigger Picture?

CEO Melinda Whittington framed the results as evidence the company is "strengthening our enterprise and increasing the agility of our business" despite a challenging consumer environment .

Key strategic highlights:

- Vertical integration advantage: ~90% of upholstered products produced in North America, which management called "a key competitive advantage" in navigating macro challenges

- Brand recognition: Named to TIME's 2026 list of America's Most Iconic Companies

- Capital allocation: Returned $24 million to shareholders ($10M dividends, $14M buybacks) with $306 million cash on hand and zero debt

The company declared a quarterly dividend of $0.242 per share, payable March 13, 2026 .

Forward Catalysts to Watch

- Q3 FY26 Earnings Call (February 18, 8:30 AM ET) — Management commentary on weather impacts and consumer trends

- Casegoods sale completion — Letter of intent signed for American Drew and Kincaid

- UK manufacturing closure — Production to cease by fiscal year end (late April)

- Joybird turnaround — Watch for stabilization in written sales as a leading indicator

Earnings call scheduled for February 18, 2026 at 8:30 AM ET. This analysis will be updated with Q&A highlights after the call.